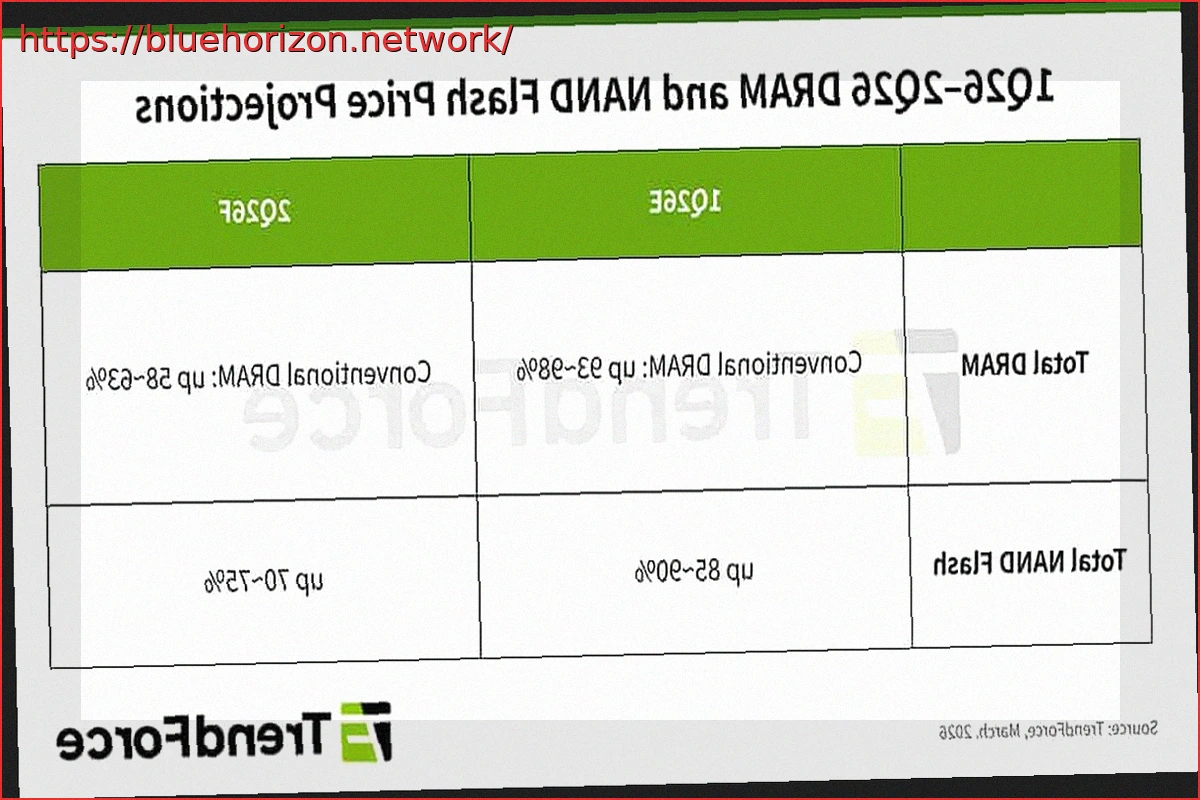

While prices for conventional DRAM and NAND Flash memory are still set to rise in the second quarter of 2026, the good news is that the pace of these increases will significantly moderate compared to the explosive first quarter. TrendForce projects quarterly increases of 58-63% for DRAM and 70-75% for NAND Flash. These figures, though still substantial, are notably lower than the 93-98% for DRAM and 85-90% for NAND Flash recorded in Q1. This slowdown offers a slight reprieve in an otherwise highly volatile pricing market.

The primary reason for this ongoing inflation stems from manufacturers’ strategies to reallocate production capacity towards higher-margin products such as HBM memory, server DRAM, and enterprise SSDs.

Memory Price Hikes Expected to Slow Down for Both DRAM and NAND Flash

In the DRAM segment, “catch-up pricing” aims to balance prices across different segments. Despite a downward revision in PC demand, suppliers have reduced shipments to OEMs, forcing buyers to acquire smaller volumes at higher prices. Server DRAM demand remains driven by Artificial Intelligence, with North American Cloud Service Providers (CSPs) accelerating inference deployments, which boosts the need for both AI servers and general-purpose servers.

RDIMM and NAND Flash Remain Key Drivers of the Issue

High-capacity RDIMMs are a key purchasing focus, and suppliers are prioritizing their production due to profitability. Long-term agreements are being negotiated to secure future supply, although short-term availability remains very tight. Regarding NAND Flash, demand for enterprise SSDs for generative AI is unstoppable. TrendForce predicts a clear shortage for 2026, with significant capacity expansion not expected until late 2027 or 2028. This leads CSPs to accept higher prices and sign Long-Term Supply Agreements (LTAs), further solidifying manufacturers’ negotiating power.

Although the market has moved past the “wildest” phase of price escalation, memory remains expensive and will continue its upward trend, albeit at a less dizzying pace. AI will continue to be the dominant factor determining capacity allocation, pricing, and delivery timelines. Despite everything, this moderation represents “good news” in the context of previous forecasts.