The conflict involving Iran has introduced a new challenge for the semiconductor industry, this time centered on the supply of helium. Despite a ceasefire agreement between Iran and the U.S. ensuring safe passage through the Strait of Hormuz, Ras Laffan in Qatar—a key industrial city and helium supplier—has remained largely out of service following attacks in early March. This disruption has reportedly cut global helium supply by 27% to 30%, pushing spot prices up by 40% to 100% within weeks, creating significant pressure on chip manufacturers in South Korea, Japan, and Taiwan.

The impact of this situation varies significantly across countries and companies, as highlighted by TrendForce. The analysis reveals how this geopolitical event is set to influence the semiconductor sector and future hardware development.

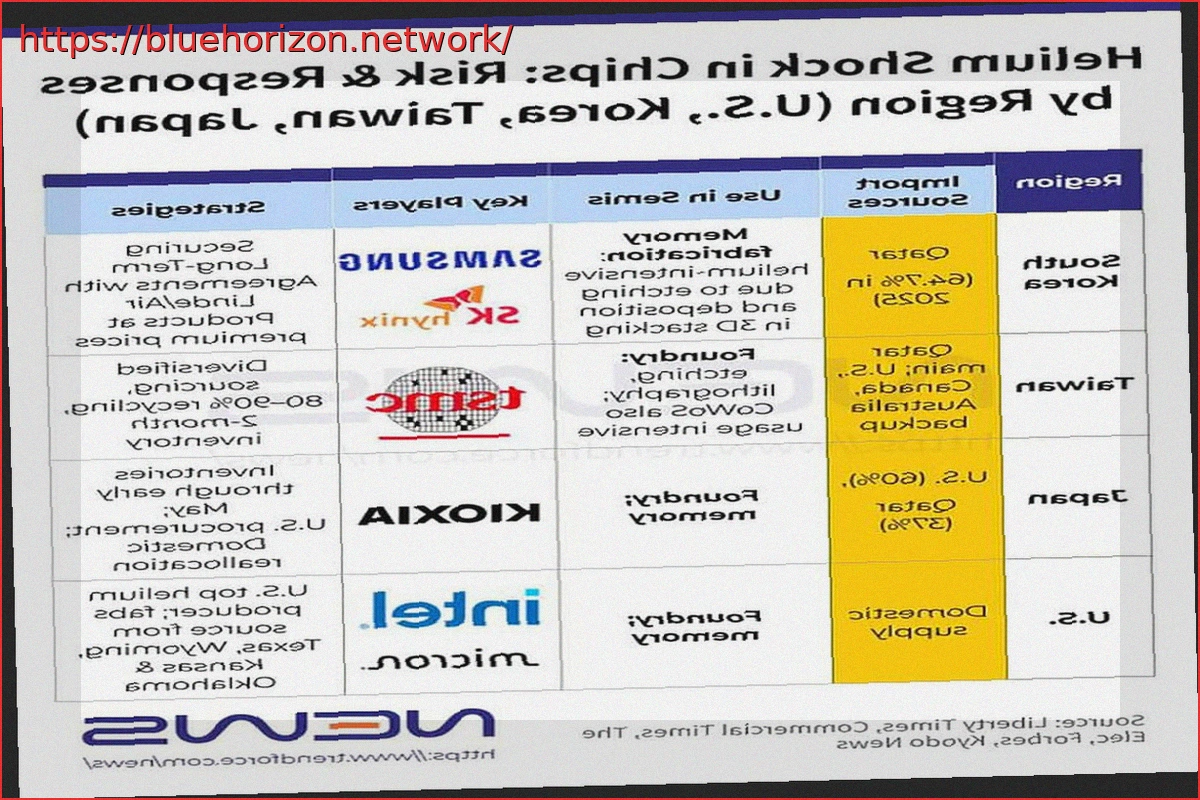

The Geopolitical Chessboard: Helium for Chips in South Korea, Taiwan, and Japan

South Korea emerges as one of the most sensitive points among chip-producing nations. In 2025, 64.7% of the helium imported by the country originated from Qatar, placing Samsung and SK Hynix in a precarious position given the complications in Gulf supply. Helium consumption is substantial in memory manufacturing, particularly in etching and deposition processes critical for 3D stacking.

South Korea’s response has been direct: diversifying suppliers, increasing recycling efforts, reallocating purchases, and securing new long-term agreements with Linde and Air Products, even at higher prices. Furthermore, the South Korean government has reportedly secured approximately four months’ worth of semiconductor-grade helium, with no immediate supply interruptions reported.

Taiwan is also exposed, though with greater room for maneuver. Helium constitutes less than 1% of wafer manufacturing costs but remains indispensable for etching, process cooling, gas purging, leak detection, and EUV lithography. On April 2nd, prices for 6N electronic helium and EUV-grade helium rose by over 5%.

TSMC stands out with its CoWoS lines being particularly sensitive to helium usage. However, the company benefits from a diversified supply chain, high on-site recycling rates (80% to 90%) in advanced fabs, and an inventory buffer of over two months.

Japan: Less Affected Due to U.S. Supply

Japan occupies an intermediate position compared to Taiwan and South Korea. In 2025, roughly 60% of its helium imports came from the U.S. and about 37% from Qatar. The Ministry of Economy, Trade and Industry has indicated that current stocks would last until early May, while the country actively seeks additional volumes from the U.S., and some domestic companies are reordering to prioritize internal market needs. Kioxia acknowledges that helium is difficult to substitute and essential for chip manufacturing.

The United States plays a different game. TrendForce positions Intel among the manufacturers with a better relative buffer against this tension because the U.S. is the world’s largest helium producer, yielding about 81 million cubic meters annually. Many local fabs are supplied from domestic sources in Texas, Wyoming, Kansas, and Oklahoma.

While Asia scrambles to fill the gap left by Qatar, Intel benefits from a significantly more stable domestic supply base, leading to some speculation in the sector regarding the motivations behind the conflict. In a crisis stemming from the Iran conflict, this disparity weighs much more heavily than it seemed just weeks ago. If not resolved quickly, the disruption in helium for chips could have critical consequences, especially for South Korea, Taiwan, and to a lesser extent, Japan.