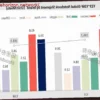

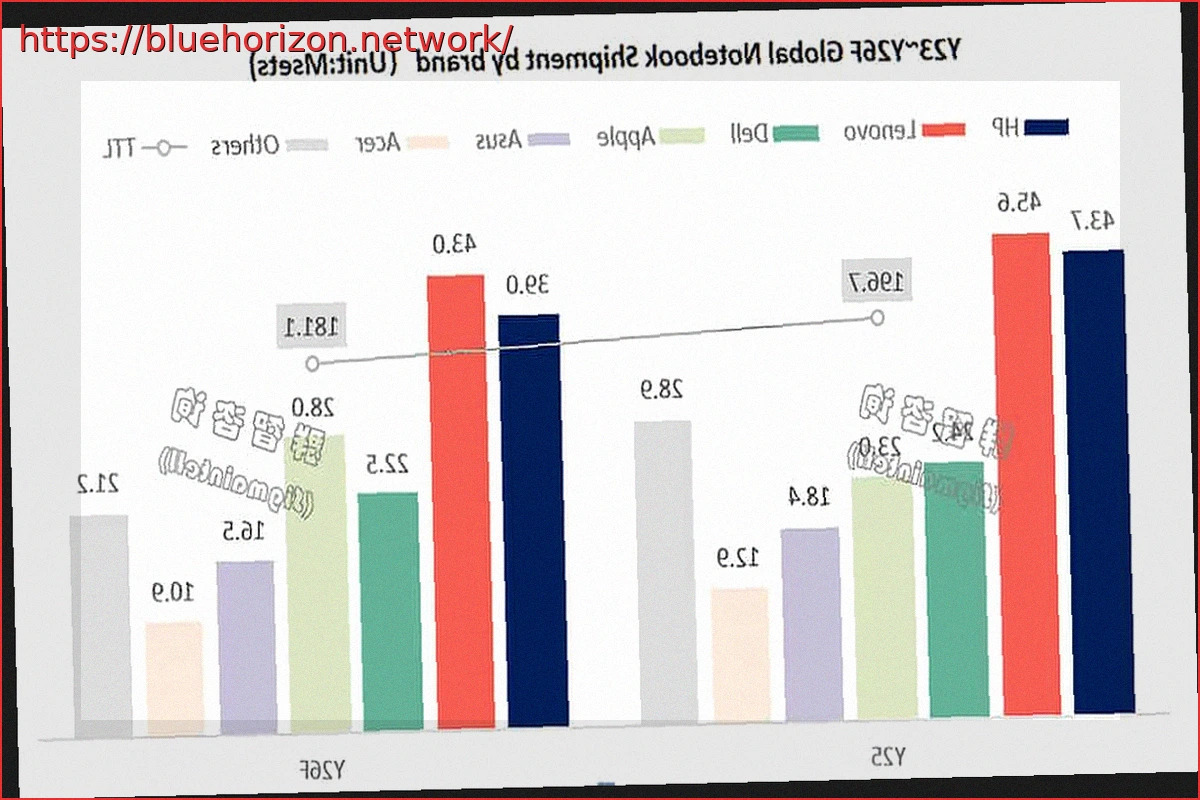

The global laptop market is bracing for 2026 with projected lower shipment volumes for nearly all major manufacturers. While this trend has been discussed previously, a new, precise report offers a clearer picture. Sigmaintell’s data compares brand shipments between 2025 and projections for 2026, revealing a market contraction from 196.7 million to 181.1 million units. The most striking aspect is the divergence in performance: only Apple is poised for growth, while the rest of the industry faces a downturn.

Amidst this shifting landscape, Apple, one of the few companies utilizing Arm architecture in this sector, is expected to be the only one to achieve year-over-year shipment growth. In stark contrast, Lenovo, HP, Dell, ASUS, Acer, and the collective group of “other” manufacturers are all predicted to experience decreases, some of which could be quite substantial.

Apple Stands Alone as the Only Top Company Projected to Boost Laptop Shipments

The anticipated success of a potential MacBook Neo, with its attractive pricing and compelling features, likely plays a significant role in Apple’s projected growth. The report also indicates a notable shift in brand ranking, with Apple expected to surpass Dell in shipment volume. While Lenovo is projected to retain its position as the brand with the highest number of shipments in 2026, its volume will decrease from 2025 levels, highlighting Apple’s rapid approach.

Lenovo’s shipments are expected to drop from 45.6 million to 43.0 million units, a decline that, while not as severe as some others, signifies a lack of growth. HP, maintaining its second-place position, is also predicted to see a decrease, from 43.7 million to 39.0 million units. Dell is forecast to lose market share, with shipments falling from 24.2 million to 22.5 million units.

Conversely, Apple’s shipments are projected to rise from 23.0 million to 28.0 million units. This significant increase is expected to propel Apple into third place in the global laptop market, a development that has broader implications for chip demand and potential cost efficiencies with manufacturers like TSMC.

The Market Faces an Inevitable Downturn Driven by AI and Economic Factors

Apple’s individual success story becomes even more pronounced when considering the overall market trend. The total market shipments, marked as “TTL” in the chart, are forecast to decline from 196.7 million units in 2025 to 181.1 million in 2026. This represents a reduction of 15.6 million units in just one year, a significant drop of approximately 7.93%. Within this general decline, Lenovo is expected to lose 2.6 million units, HP 4.7 million, and Dell 1.7 million.

ASUS is also predicted to experience a downturn, with shipments falling from 18.4 million to 16.5 million units, a decrease of 1.9 million. Acer’s shipments are projected to drop from 12.9 million to 10.9 million, a cut of 2.0 million units. In contrast, Apple’s trajectory is sharply upward. The brand is expected to increase its laptop shipments from 23.0 million to 28.0 million, adding 5.0 million units year-over-year. This represents the largest absolute growth among the major brands featured in the chart, and it occurs during a period when all other major players are expected to falter.

The data also highlights a substantial decline in the “other manufacturers” category, which is projected to fall from 28.9 million units in 2025 to 21.2 million in 2026, a decrease of 7.7 million units. This is the most significant absolute reduction across the board. Therefore, while major brands are experiencing losses, they are generally less severe than those affecting smaller manufacturers. Apple appears to be the only one capable of thriving, while the overall market faces a near double-digit contraction. It remains to be seen in December if these projections hold true, prove inaccurate, or are even surpassed by a more severe market contraction.