The NAND Flash memory market is entering a new phase of extreme pressure, portending further price increases. According to the latest data from consultancy TrendForce, major NAND manufacturers will barely add new production capacity throughout 2026. This comes despite the growing demand from AI servers absorbing an increasing portion of available output. The consequence is clear: the firm anticipates supply shortages to persist all year, resulting in continued price hikes for SSDs.

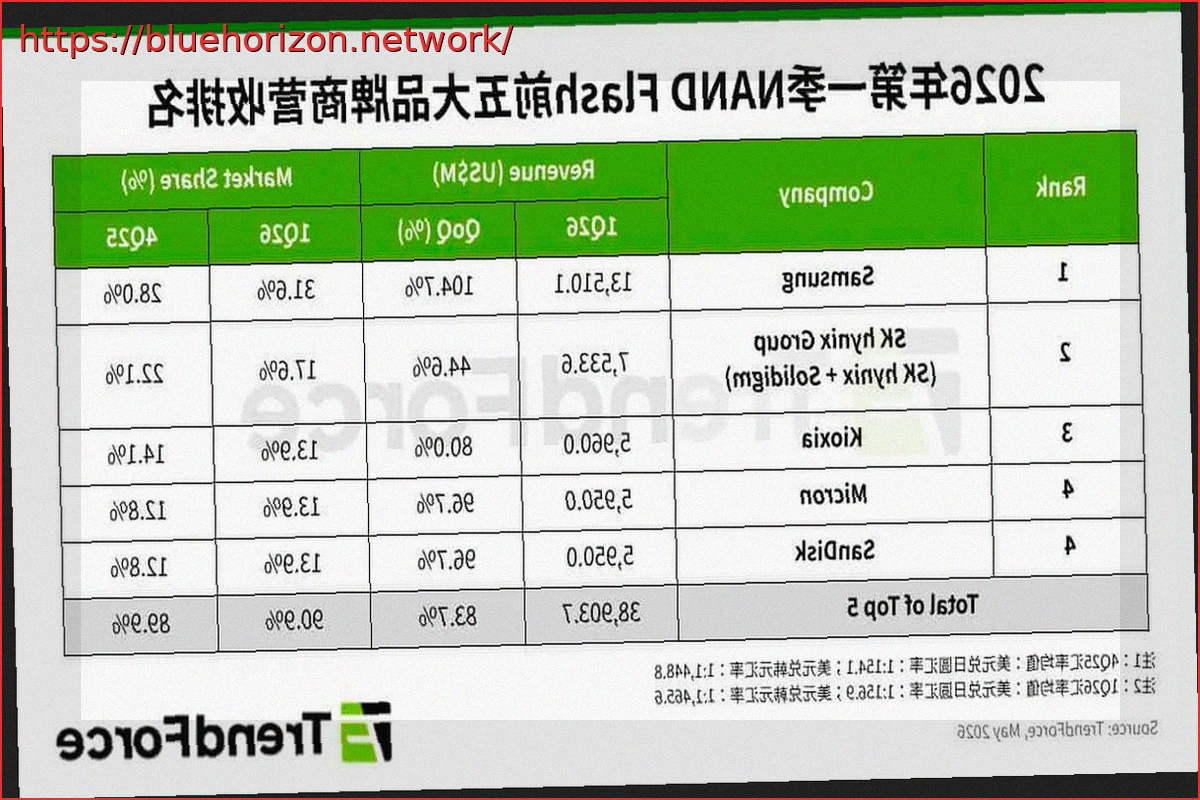

The most striking figure is revenue. In the first quarter of 2026, the top five global NAND Flash suppliers collectively generated over $38.9 billion in revenue, an 83.7% increase from the previous quarter. This isn’t just due to selling more chips; the average selling price has significantly exceeded forecasts due to a combination of explosive demand and limited supply. Naturally, if scarcity is engineered, prices continue to climb – a situation mirroring the DRAM market.

Most NAND Memory Manufacturers Nearly Doubled Their Quarterly Revenue

Samsung led the market with $13.51 billion in NAND revenue during the first quarter, a 104.7% surge that boosted its market share from 28% to 31.6%. SK Hynix Group, including Solidigm, secured second place with $7.53 billion, a 44.6% increase, driven particularly by high-capacity enterprise QLC SSD orders. Kioxia achieved $5.96 billion, an 80% rise, while Micron and SanDisk tied with approximately $5.95 billion each, both experiencing 96.7% growth.

SanDisk’s performance is particularly noteworthy. TrendForce highlights that its data center business grew by over 200% quarter-over-quarter, reinforcing the shift in NAND market value from traditional consumer products (PCs, smartphones, USB drives, home SSDs) towards higher-margin enterprise solutions. Manufacturers have clear incentives to prioritize servers and data centers over cheaper consumer products.

This mirrors the trend in DRAM. Manufacturers are avoiding production increases by diverting NAND memory production from consumer use to enterprise, data centers, servers, and AI applications. The benefit is twofold: significantly higher profits from these sectors while consumer markets face price increases due to artificial scarcity driven by reduced production for more lucrative markets.

NAND Memory Has Also Become a Strategic Resource: Prepare to Pay More

TrendForce indicates that the weakness in the smartphone and PC markets in the second quarter of 2026 will not be enough to ease the market. Although the rising cost of memory and final products may curb some consumer demand, server orders are filling that gap. In other words, even if fewer consumer devices are sold or some manufacturers reduce base capacities, data center demand will continue to absorb available capacity.

This explains why contract prices for NAND Flash are expected to continue their strong upward trend. In a previous forecast for the second quarter of 2026, TrendForce estimated NAND Flash memory prices would rise between 70% and 75% compared to the previous quarter. Conventional DRAM, meanwhile, was projected to increase by 58% to 63%. The firm itself noted that NAND capacity is increasingly being allocated to enterprise SSDs, putting greater cost pressure on consumer applications.

The situation also has a clear implication for end-users. Cheaper SSDs (1TB, 2TB, or 4TB) will take a considerable time to return to normal prices, as the bottleneck is not merely temporary. The industry can improve bits produced through more advanced nodes, more layers, and QLC technology. However, TrendForce warns that significant capacity expansion is unlikely before late 2027 or even 2028.